As an owner, you should consistently ask yourself how well are your accounting goals working each month and have you effectively monitored your performance? A successful owner will have a business to-do list; bookkeeping and accounting should be an integral part.

Having a degree is not a pre-requisite for running a business. Rather than spending time on tedious accounting, most business owners focus more of their attention on what got them into business in the first place. Don’t let improper bookkeeping and inaccurate records affect your compliance or shut your doors. This year, lets set accounting goals to put your business in a profitable direction!

First, its best to have an understanding of how the three most important qualities of accounting affect your business.

Accounting provides a clear picture of how well your business operates currently or in the past to the users of the information, such as decision makers and investor.

It measures pervasive constraints, such as the benefits or costs of new product or service lines, investment projects, or purchases.

It increases the user’s ability to make useful decisions, strategic changes, and accurately forecast future performance based on the reliability of your financial data. Depending on your business, every accounting cycle varies. Your financial information is a reflection of how well you maintain your accounting cycle on a consistent basis, and how you set your previous goals.

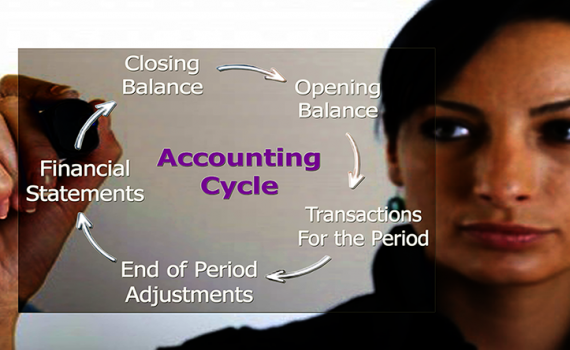

In order to set the proper bookkeeping and accounting goals, you must have a thorough understanding of the Accounting Cycle, and make your goals relevant, reliable, and measurable according to GAAP or IFRS accounting Standards. In addition, important metrics should be set to monitor your progress, based on your industry

The Accounting Cycle is the sequence of accounting procedures completed during each accounting period and includes:

- Recording Transactions

- Identifying and Analyzing Business Transactions

- Recording Journal Entries

- Posting to the Ledger

- Unadjusted Trial Balance

- Recording Journal Entries

- Adjusting Entries

- Adjusted Trial Balance

- Financial Statements

- Closing Entries.

Internal controls and a durable bookkeeping system or robust accounting software can help to alleviate the hassle of maintaining outdated templates, plus save you time. As a business person, you want to be able to gauge your profit or loss, revenue and expense accounts, and bank reconciliations from cycle to cycle in order to achieve the highest level of accuracy with your financial reporting.

The PMC Team